Mar 31, 2009

Mar 28, 2009

Globalize My Homework!

Raise your hand if you saw this coming. Many anonymous people in Vietnam, China and Sri Lanka are already making clothing and iPod's for your students. Doesn't it make sense when they start making papers for your students as well?

Raise your hand if you saw this coming. Many anonymous people in Vietnam, China and Sri Lanka are already making clothing and iPod's for your students. Doesn't it make sense when they start making papers for your students as well?SSEIN1: The student will explain why individuals, businesses, and governments trade goods and services.

...and if they don't want to explain this themselves they can always pay someone in Indonesia $19.99 to do it for them!

Mar 26, 2009

A Corner Turned?

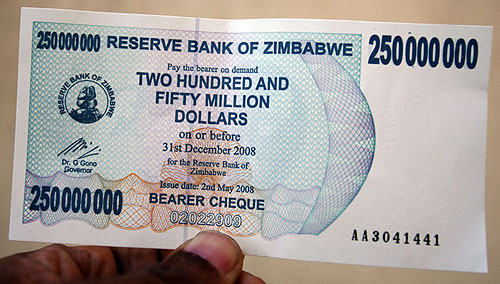

Perhaps things are looking up in Zimbabwe. They have recently ditched their dollar (look here to see what they are doing with the old dollars) and are now using foreign currencies as legal tender. The price level actually dropped a tad last month in that country. A bit of good news for a nation that was recently experiencing an inflation rate of roughly 231 million percent.

Perhaps things are looking up in Zimbabwe. They have recently ditched their dollar (look here to see what they are doing with the old dollars) and are now using foreign currencies as legal tender. The price level actually dropped a tad last month in that country. A bit of good news for a nation that was recently experiencing an inflation rate of roughly 231 million percent.I was having a conversation with an elementary school teacher today and she told me that one of her students asked her the "Why can't we just print more money?" question that all of us get from time to time. These photos offer a good explanation I think.

Mar 25, 2009

From the Classroom volume 13

In the words of College Gameday’s Lee Corso, “Not so fast my friend.” Your work is not yet done.

Just when you think your kids have it and they understand fiscal and monetary policy, someone asks a question that lets you know that they still have no clue how the Fed or Congress might respond to specific economic problems. So I now use this activity* (heavily borrowed from a Fed workshop) as one of the final assignments in my Macro unit. It brings together all the elements. Students have to diagnose problems in the economy and prescribe a remedy for both Congress and the Fed. And just in case your students are getting cocky, they are even thrown a curveball on how to battle stagflation using monetary policy. - Melvin

*Send an email to gcemrrx@langate.gsu.edu if you would like a copy of this activity. Someone with way more technological skill than I would know how to attach a Word document to this post. Sadly, I am not that person- Mike Raymer

Mar 23, 2009

A Big Pile of $$$$

This website has many great visuals that attempt to explain the current economic "situation." You can look here to see where all the $$$ went. This lets you compare the cost of the $700 billion dollar bailout to the cost of the Iraq war. Examine this one to compare government actions during past recessions.

This website has many great visuals that attempt to explain the current economic "situation." You can look here to see where all the $$$ went. This lets you compare the cost of the $700 billion dollar bailout to the cost of the Iraq war. Examine this one to compare government actions during past recessions.Which brings me here. Show the kids this one. I guarantee at least one of your students will say, "Holy ..... (something)!" when they see that last visual. That is one large pile of cash.

How many students do you have in your class? Probably around 27 right? Assign one visual to each student and have each student explain the visual to the class. Might be fun and informative.

Mar 21, 2009

2009 Economics Challenge Champions

Congratulations to our 2009 Economics Challenge winners.

Congratulations to our 2009 Economics Challenge winners.David Ricardo Division: Starr's Mill High School from Fayette County.

Adam Smith Division: Parkview High School from Gwinnett County.

Both teams advance to the Regional Championships that will take place on April 27th at the Federal Reserve Bank of Atlanta. Good luck to the Panthers that wear Columbia blue and black and the Panthers that wear orange!

A huge thank you to all of the teams, coaches and judges that came out to GPB this morning. The Georgia Council could not have pulled this off without your help and support.

Mar 20, 2009

The Opportunity Cost of Your Bracket

NCAA March Madness. Why every other collegiate sport in the universe does not go to something like this is beyond me. America sure loves college hoops this time of year. As for me, I would rather watch this than some big conference hoops power squash some tiny school nobody has heard of by 56 points. (I'm looking at you UConn!) But I digress. Did any of you sneak a peek at the tv during work yesterday? If so, you were not alone. Go ahead and read this but then GET BACK TO WORK!

SSEF1: d. Define opportunity cost as the next best alternative given up when individuals, businesses and governments confront scarcity by making choices.

SSEF6: a. Define productivity as the relationship of inputs to outputs.

SSERAYMER1: a. Explain the difference between Sweet 16 and Elite 8.

Mar 19, 2009

The Commanding Heights

Seven years ago PBS released the outstanding, and incredibly informative, six-hour documentary called Commanding Heights: The Battle for the World Economy. The series, based on the book written by Daniel Yergin and Joseph Stanislaw, follows the trajectory of free markets in the 20th century. Taking its title from a speech given by this guy, Commanding Heights examines capitalism, globalization and the world economy from the early 1900's until the late 1990's.

Seven years ago PBS released the outstanding, and incredibly informative, six-hour documentary called Commanding Heights: The Battle for the World Economy. The series, based on the book written by Daniel Yergin and Joseph Stanislaw, follows the trajectory of free markets in the 20th century. Taking its title from a speech given by this guy, Commanding Heights examines capitalism, globalization and the world economy from the early 1900's until the late 1990's. Whenever I am asked to recommend additional resources for teaching economics I always plug the Commanding Heights book and documentary. After reading the book and watching the series you will have a much stronger understanding of the workings of the global economy over the course of the last one hundred years.

To supplement the reading and documentary you can also visit the Commanding Heights website. Here you will find lesson plan ideas, video clips, time lines and many other useful bits of information that will help you in the classroom. Show your students the hyperinflation clip on Bolivia and they will have a much greater understanding of the implications of a 50,000% inflation rate.

Mar 18, 2009

$1,000,000,000,000.00

Would any of you like to help me out? Do you think you could compile a list of all of the Fed programs currently in place? You know, all of the new strategies they have come up with since October of 2008. Way back in the day (the beginning of this school year) the Fed had what, three tools to conduct monetary policy? ...and they didn't even use one of those three. Now it seems like we get something new each week.

Would any of you like to help me out? Do you think you could compile a list of all of the Fed programs currently in place? You know, all of the new strategies they have come up with since October of 2008. Way back in the day (the beginning of this school year) the Fed had what, three tools to conduct monetary policy? ...and they didn't even use one of those three. Now it seems like we get something new each week.Today they announced they are going to pump $1 TRILLION dollars into the economy. Let that sink in for a moment. One. Trillion. Dollars. As a side note, I find that it is somewhat amusing to talk like Dr. Evil when you say "$1 trillion dollars".

So if you are up to the challenge I will send a lovely GCEE umbrella to the person that comes up with the most thorough list of Fed monetary tools. Good luck.

Mar 17, 2009

Mar 16, 2009

From the Classroom vol 12

“So what if we just print off more money and not tell anyone?”

I am sure we have all had this question asked of us by our students and I am sure that many economics teachers answer it in a similar way—a trip to the dollar store to load up on cheap prizes. Costume jewelry, candy, plastic frogs, cars, stickers; the possibilities are nearly limitless. I have found that the cheesier, the better.

Conduct a couple of auction rounds, supplying a great deal more currency in round two than round one. Record the prices on the board and that first question becomes obvious to most students. Simulations like this (also located in VE3-- Focus: High School Economics and Economics in Action) seem to be a great springboard to initiate your classroom discussion of inflation.

And if any silver lining can be found in the tragedy of Zimbabwe, it is that it sure makes teaching the consequences of inflation easier to understand. It is extremely hard for even the most disinterested 17 year old to glaze over during a discussion about an exchange rate of 300 trillion to 1 or a country chopping 12 zeroes from its currency.

I am sure we have all had this question asked of us by our students and I am sure that many economics teachers answer it in a similar way—a trip to the dollar store to load up on cheap prizes. Costume jewelry, candy, plastic frogs, cars, stickers; the possibilities are nearly limitless. I have found that the cheesier, the better.

Conduct a couple of auction rounds, supplying a great deal more currency in round two than round one. Record the prices on the board and that first question becomes obvious to most students. Simulations like this (also located in VE3-- Focus: High School Economics and Economics in Action) seem to be a great springboard to initiate your classroom discussion of inflation.

And if any silver lining can be found in the tragedy of Zimbabwe, it is that it sure makes teaching the consequences of inflation easier to understand. It is extremely hard for even the most disinterested 17 year old to glaze over during a discussion about an exchange rate of 300 trillion to 1 or a country chopping 12 zeroes from its currency.

Mar 15, 2009

Mar 14, 2009

Weekend Getaway

Did your school make the list? I wonder how many of these companies offer their employees the chance to experience bus duty, fire drills and pep rallies?

Mar 13, 2009

At a workshop today some of us were talking about the "Buy American" wording in the stimulus package. My question is this- can you go a month buying only American made products? How about for a week? A day? Is it even possible? Extra credit to the first person that can go a month only purchasing things made in the USA.

At a workshop today some of us were talking about the "Buy American" wording in the stimulus package. My question is this- can you go a month buying only American made products? How about for a week? A day? Is it even possible? Extra credit to the first person that can go a month only purchasing things made in the USA.Ask your students if they can pull this off. Make it a challenge. The beauty of this is that it can open up a good discussion on the costs and benefits of "buying American" and free trade in general. What will happen to your students' overall selection of goods and services if they only buy American? Will they be paying the same prices as before? If they buy one of these and it was made in South Carolina is it "American"?

And would anyone like to explain this?

Mar 12, 2009

From the Classroom vol 11

I believe that it is relatively easy for my students to see the connection between GDP and wealth. Higher GDP means more goods and services—more flat screens, better cell phones, more restaurant quality meals, etc. They tend to dwell on just the materialistic things. Therefore, in order to help my students recognize the relationship between GDP per capita and standard of living, we get down to some old fashioned research (well, as old fashioned as an Internet search can be.)

I generate a chart which requires them to find a variety of stats (GDP per capita, literacy rates, percent of GDP from agriculture, infant mortality rate, etc) for a variety of countries. All of this information is available at the CIA World Factbook. The students are then required to draw conclusions about the relationships between GDP per capita and quality of life stats based on the information they gather.

As educators, I believe that we all value opportunities for our students to draw their own conclusions from a set of data, and I think this is a relatively pain-free (for you) way to achieve that. That is, assuming you have Internet access (that actually works) for all of your students.

I generate a chart which requires them to find a variety of stats (GDP per capita, literacy rates, percent of GDP from agriculture, infant mortality rate, etc) for a variety of countries. All of this information is available at the CIA World Factbook. The students are then required to draw conclusions about the relationships between GDP per capita and quality of life stats based on the information they gather.

As educators, I believe that we all value opportunities for our students to draw their own conclusions from a set of data, and I think this is a relatively pain-free (for you) way to achieve that. That is, assuming you have Internet access (that actually works) for all of your students.

Mar 10, 2009

The Stimulus Package (part 2)

This is the second opinion piece on the current stimulus plan. Just like yesterday’s post, the following opinion is of the author and not the Georgia Council. Today we will hear from Amy Hennessy, a teacher at Davidson Fine Arts Magnet School.

Mitigating the Downturn

Most mainstream economists have embraced the Keynesian argument that refutes Say’s law about prices and wages being completely flexible and the SRAS curve being vertical. If, as Keynes theorizes, aggregate supply will be upward sloping in the short run when there is a decrease in aggregate demand wages and prices will be sticky. As a result RGDP will decrease and a recessionary gap will emerge. We are currently facing the prospect of an estimated two trillion dollar recessionary gap.

When Okun's law is applied to the current unemployment rate as reported by the Nobel Prize winning economist Paul Krugman one can appreciate the potential implications of the stimulus plan. President Obama’s Director of OMB, Peter Orszag, in 2001 wrote a paper that referenced a study concerning the impact of unemployment compensation as an automatic stabilizer helping to mitigate the full impact of a drop off in aggregate demand. He and Nobel Prize winning economist Joseph Stiglitz authored a paper in 2001 arguing in favor of spending increases over continued tax decreases. Even though monetary policy actions have come to guide most macro policymaking actions over the past few decades, we are now facing the prospect of a liquidity trap and thus must turn to fiscal stimulus alternatives.

A fundamental truth about an economy in contraction is that real people are the ones having to make the agonizing choices about how to put food on the table, get their child to the doctor without any medical coverage because it disappeared with the job, and a roof over their family’s head. The American Recovery and Reinvestment Act of 2009 provides extensions for automatic stabilizers along with the discretionary spending allocated to long overdue infrastructure projects , weatherization and renewable energy projects, as well as school renovations and upgrades.

Sixty percent of respondents think the recently passed stimulus plan will modestly help the economy overcome recession. Infrastructure improvements, unemployment expansion and personal tax-rate cuts were seen as the most effective parts of the plan. (National Association for Business Economics survey)

The $787 billion economic stimulus package recently signed into law should increase demand and production over the next two years, Mr. Bernanke said, before adding that “the timing and the magnitude of the macroeconomic effects of the fiscal program are subject to considerable uncertainty.” Even as the stimulus plan seeks to lay the groundwork for self-sustaining recovery, he said, this would depend heavily on a return to financial stability. And on that front, he said, “more needs to be done.”

The federal budget will provide some support to the economy in 2009 and 2010, even in the absence of any new stimulus legislation. Federal tax liabilities (and therefore revenues) fall proportionately more than incomes in recessions, and that additional drop dampens the decline in households’ real after-tax spending power. In addition, spending on some programs, such as those providing unemployment insurance and the Supplemental Nutrition Assistance Program (formerly known as the Food Stamp program), automatically increases during recessions. Those recession-induced changes in the federal budget tend to smooth out economic cycles. The magnitude of those “automatic stabilizers” can be only roughly estimated, but in CBO’s forecast about $250 billion of the change in the deficit (about 1.8 percent of GDP)between 2008 and 2009 appears to be attributable to them.1 In contrast, spending by state and local governments will only mildly ease the downturn in economic activity.

In response to lower-than-expected revenues and requirements for balanced budgets, they are cutting back their spending on goods and services, and CBO’s forecast assumes essentially no real growth in that spending this year. Total state and local deficits (including both the operating and the capital accounts) will increase, but the change in the total deficits will be small relative to the recession-induced change in the federal deficit. A major source of uncertainty in the outlook is the degree and persistence of turmoil in financial markets and the resulting impact on the future course of the economy.

Many financial instruments and practices that contributed to the financial crisis came into widespread use only in the past decade, and the scale of the problems and the worldwide linkages of financial markets are significantly different from what they were in previous episodes of financial stress in the United States. Furthermore, the scale and novelty of federal intervention, particularly by the Federal Reserve, and uncertainty about the degree to which those interventions will affect the economic outlook, make it particularly difficult for analysts to use historical patterns to forecast the near future. (From report of the Congressional Budget Office.)

NYT's David Leonhardt "...for all the criticism the stimulus package has been getting, it does pretty well by several important yardsticks. First of all, the package really is stimulus. It will quickly give money to the people who have been hardest hit by the recession and who, not coincidentally, will be most likely to spend that money soon. The spending also has a chance to do some long-term good, by paying for the computerization of medical records, the weatherization of homes and other such investments...”

“The only way to increase aggregate demand is going to be through” government spending on roads, bridges and other infrastructure, Roubini said at a Bloomberg conference in New York. “We need a huge plan… (NYU Professor of economics Nouriel Roubini, a man who has been vindicated for his prognostications that had been widely disregarded by many in the mainstream prior to this meltdown.)

Joseph Stiglitz also noted that the previous stimulus did little to address the rise in foreclosures in the United States, which he said was central to the economic crisis. He also said solving the “crisis” outweighed any concerns over deficit spending and the national debt. The Nobel Prize winner also said people are only looking at one side of the nation’s balance sheet, the liability side and ignoring the asset side. According to Stiglitz, the assets the government will accrue, no matter how illiquid they are, will offset the huge debt liabilities the Obama administration would run up with a stimulus project. “The deficit is only one side of a country’s balance sheet – it’s the liability,” Stiglitz said. “We also have to look at the asset side and that’s why he’s been emphasizing not only that we borrow, but we use it to buy assets that increase the asset side of our balance sheet.”

The Stimulus Package (part 1)

Over the next two days I will be posting the opinions of two different teachers; one opposed to the stimulus, the other in support. Both opinions are of the authors and not the Georgia Council. Today we will hear from Marc Mayfield, a teacher at LaGrange High School.

Over the next two days I will be posting the opinions of two different teachers; one opposed to the stimulus, the other in support. Both opinions are of the authors and not the Georgia Council. Today we will hear from Marc Mayfield, a teacher at LaGrange High School.The Stimulus Bill Will Not Work: A Free Market Perspective

To understand why the stimulus bill will fail, it is necessary to understand how the economy got into its current predicament. Our current recession began in December 2007, according to the National Bureau of Economic Research. It had become obvious to many economy watchers that the

When the recession became official, it surprised a lot policymakers and politicians who do not understand monetary policy, fiscal policy, business cycles, or the role of the Fed. The stated purpose of the Federal Reserve is to promote economic growth and stability. The Federal Reserve’s Board of Governors is willing to do virtually anything to prevent an economic downturn from occurring. This includes preventing necessary market corrections and adjustments from taking place in a timely manner. The Fed has the ability to use the printing press to paper over a crisis and keep a bubble from popping in the short run. However, this only serves to make the unavoidable market correction longer and sharper than it otherwise would have been.

The roots of the current crisis are rooted in monetary policy decisions pursued by Greenspan’s Fed from November 2002 when rates were cut to 1.25%, followed by the June 2003 cut to 1.00% where it stayed until rates began rising in June 2004. These historically low rates led to a large amount of malinvestments by businesses that would have to be liquated at some point in the future.

New Federal Reserve Chairman Ben Bernanke began to sense a coming liquidation of the malinvestments in the summer of 2007. The Fed began slashing interest rates in September 2007 from 5.25% until they reached the new unheard of target level of 0.0% to 0.25% in December 2008. This was a failed attempt to prevent a necessary market correction from occurring. The Fed’s monetary policy failed to avert this recession and may have sown the seeds for the next recession in the process.

So in the summer of 2007, instead of allowing the market to correct, the Fed began pouring drinks. What we had was a classic Hayekian Hangover.[1] This is the opposite of what should have been done. A sharp, short recession could have cleared the economy of the malinvestments created during the period of November 2002 until June 2004. The necessary correction would have set the stage for a period of strong sustainable growth. Instead the Federal Reserve began slashing interest rates (more easy money) and set the stage for a far more severe recession.

Add to the mismanagement of interest rates by the Fed a financial crisis and a housing crisis and you have set the stage for one of the worst economic downturns in the post-World War II era. In March 2008, Bear Stearns collapsed. The Fed and JP Morgan step in to bailout an investment bank. Jim Rogers appeared as the voice of reason when he declared, “If you bail out every investment bank that gets in trouble, that's not capitalism, that's socialism for the rich.” Unfortunately, nobody was willing to take

Bear Stearns failed because:

“of the poor judgment of their management: their aggressive risk taking, their positions in the mortgage back market, their apparent lack of risk controls, their leverage, lack of liquidity and reserves, and the enemies they made over the years.”[2]

Fannie Mae and Freddie Mac go under in the fall of 2008 as the housing bubble pops. Then Lehman Brothers falls in September. Apparently they were not worthy of a bailout. The Fed continued to cut interest rates in a vain attempt to stop the bleeding. In December, the National Bureau of Economic Research confirmed what everyone already knew, the economy was in a recession.

While the Fed was busy cutting rates, there was an election and we got a new president who promised change. For the Obama administration, since monetary policy had obviously failed to prevent the recession, or to moderate its severity, it seemed time to give fiscal policy a turn. In my opinion economic stimulus packages do not work. A country cannot spend itself into prosperity. Expansionary fiscal policy is the wrong solution for a recession for practical, historical, and theoretical reasons. Fiscal policy is ineffective in addressing a recession for the following reasons:

1. Fiscal Policy Time Lags

2. Fiscal Policy Ignores the Lessons of History

3. Fiscal Policy Ignores Budget Realities

4. Fiscal Policy Misdiagnoses the Problems

1. Fiscal Policy Time Lags

Even if you concede that a government can tax, spend, and borrow a nation into prosperity, expansionary fiscal policy remedies are too slow to have the intended consequences. By the time a recession is identified and “appropriate” legislation is drafted and debated, the crisis has generally passed.

Here I am being generous and assuming the current stimulus is well thought-out necessary spending. The current stimulus package is none of those things. It is a grab bag of pork projects and unrelated spending having little to do with building a solid foundation for future economic growth and prosperity. There is not time or space to devote to describing the pork-laden stimulus package.[3]

2. History: Depression of 1920-21 and

The Recession of 1920-1921 was severe. GDP dropped 24%. Unemployment more than doubled to 4.9 million. However, Harding did not panic. He acted calmly and rationally to confront the problems.

Harding attacked the bloated federal budget: spending was cut from $6.3 billion in 1920 to $3.2 billion in 1922. There were also massive cuts in tax revenue. Tax revenue declined from $6.6 billion in 1920 to $4 billion in 1922. The massive reduction in the size and scope of government allowed the national debt to be cut significantly.

According to Richard Vedder and Lowell Galloway the roaring 1920s “were arguably the brightest period in the economic history of the

The massive amounts of spending failed to achieve the desired results. “This has led many to conclude that spending did little more than sink

3. Fiscal Policy Ignores Budget Realities

We have a national debt that will soon hit $11 trillion dollars.[7] We are going into debt at the rate of $3.71 billion dollars a day. This is not a sustainable trend. Our current Debt-to GDP ratio is 75% of our $14.3 trillion dollar economy. We need to reduce this figure, not increase it.

FY 2008 was a disaster from the stand point of fiscal responsibility. FY 2009 is the year we break the $3 trillion budget barrier. In all likelihood it will surpass $4 trillion. This fiscal insanity is going to saddle taxpayers with a tremendous burden and future generations with a national debt that can never be eliminated.

Some will notice the “cuts” in the FY 2010 budget. This is largely an illusion. Comparisons should not be made on the outlier FY 2009 budget, but to the pre-crisis FY 2008. This phenomenon is known as the “ratchet-effect.” Government spending increases in response to a “crisis” and spending explodes. After the crisis is over, spending is cut but never to the pre-crisis levels.

Why does this matter? Government creates nothing. Everything the government has is extracted from the private economy by taxing, borrowing, or inflating. All three sources have a negative impact on the economy.

According to Tim Geithner, “Failure to reduce deficits to this level would result in higher interest rates as government borrowing crowds out private investment, leading to slower growth and lower living standards for Americans.”

4. Fiscal Policy Misdiagnoses the Problems

The cause of a recession is not a lack of spending. It is malinvestments that occurred in the boom phase of the business cycle. It is a myth that we can spend ourselves into prosperity. Consumption does not create prosperity. Consumption is the result of prosperity. It is savings and investment that drive the economy and create economic growth.

The business cycle is just that a cycle. Once the boom occurs the bust is inevitable. A recession is simply a market correction, where businesses address mistakes and put their financial house back in order. Government intervention only delays the inevitable.

Hans Sennholz reminds us, “A recession is a time of readjustment and recovery when businessmen correct the mistakes made in the past and put their houses back in order. It is an integral part of a business cycle that begins with a boom, leads to a bust, and ends with recovery.”[8]

Conclusion

The current recession is the direct result of the interventions of the Federal Reserve under Alan Greenspan and Ben Bernanke. Rather than allow the for the necessary market corrections to occur in 2002-2003, they papered over the crisis and ensured that when the housing bubble finally popped, that it would be severe.

The recovery that will inevitably occur will be in spite of government inventions into the economy, not because of them. Unfortunately recovery will occur months if not years later than if should have because government intervention has prevented markets from adjusting.

Murray Rothbard identified the best course of action for dealing with a recession in his classic essay “Economic Depression: Their Cause and Cure”:

The depression is the process by which the market economy adjusts, throws off the excesses and distortions of the previous inflationary boom, and reestablishes a sound economic condition.

The depression is the unpleasant but necessary reaction to the distortions and excesses of the previous boom. The business cycle is brought about, not by any mysterious failings of the free market economy, but quite the opposite: By systematic intervention by government in the market process. Government intervention brings about bank expansion and inflation, and, when the inflation comes to an end, the subsequent depression-adjustment comes into play.

What the government should do, according to the Misesian analysis of the depression, is absolutely nothing. It should, from the point of view of economic health and ending the depression as quickly as possible, maintain a strict hands off, "laissez-faire" policy. Anything it does will delay and obstruct the adjustment process of the market; the less it does, the more rapidly will the market adjustment process do its work, and sound economic recovery ensue.[9]

[1] A Hayekian Hangover, http://www.cato.org/research/articles/hanke-020626.html and A Classic Hayekian Hangover http://www.auburn.edu/~garriro/hangover.htm

[2] source: Barry Ritholtz, http://bigpicture.typepad.com/comments/2008/03/who-is-to-blame.html

[3] Here’s What $800 Billion Buys Today http://www.reason.com/news/show/131694.html and Why the Stimulus Plan Won’t Work http://www.reason.com/news/show/131661.html

[4]

[5]

[6] ibid.

[7] 10,947,934,941,039 on

[9] Murray Rothbard, http://mises.org/story/3127

Mar 7, 2009

The Blame Game

I believe it was Canadian rocker Tom Cochrane who said, "We know you've got to blame someone." I mention this because while I'm out and about doing workshops all over Georgia I am often asked who is to blame for our current financial mess. I always say it was a guy named Frank from Peoria, Illinois. Seems as plausible as any other answer I can think of on short notice.

I believe it was Canadian rocker Tom Cochrane who said, "We know you've got to blame someone." I mention this because while I'm out and about doing workshops all over Georgia I am often asked who is to blame for our current financial mess. I always say it was a guy named Frank from Peoria, Illinois. Seems as plausible as any other answer I can think of on short notice.So who do you think is to blame? Not such an easy question to answer is it? TIME magazine tried to answer the question and the result is this list of 25 people. Anyone missing?

Mar 6, 2009

Spring (econ) Training

Spring is definitely in the air. The daffodils* are blooming, the birds are flying back into town and the sound of excited teens chattering about the Econ Challenge is filling high schools from Augusta to Alpharetta. With spring comes spring training. No, I'm not talking about this spring training, I'm talking about THIS spring training. That's right, it is almost time for the 3rd Annual Economics Challenge Championship.

Spring is definitely in the air. The daffodils* are blooming, the birds are flying back into town and the sound of excited teens chattering about the Econ Challenge is filling high schools from Augusta to Alpharetta. With spring comes spring training. No, I'm not talking about this spring training, I'm talking about THIS spring training. That's right, it is almost time for the 3rd Annual Economics Challenge Championship.At Parkview, Coach Petmecky has his teams involved in two-a-days; micro in the morning, macro in the afternoon. Whitewater coach Sewall has her team training in some undisclosed location. Rumor has it the Starr's Mill contingent is working with a team of Russian economists and word on the street says defending champ Davidson Fine Arts has been training since early September of 2008.

This year is going to be big. A total of 18 teams will be competing for trophies, savings bonds, a chance to move on to regionals and pride. Good luck to everyone.

*And who knew there was an American Daffodil Society?

Mar 5, 2009

From the Classroom vol 10

For me, the Macroeconomics unit must begin with a discussion of GDP. I find it useful to borrow elements of Lesson 33 “Gross Domestic Product and How to Measure it” of the Capstone book located conveniently on VE3.

This lesson supplies a good estimation of different sectors of GDP, but the part I have found most useful is the student activity. Working in groups, the students figure out how events affect GDP. My students have found this activity extremely beneficial to them in the past.

This lesson supplies a good estimation of different sectors of GDP, but the part I have found most useful is the student activity. Working in groups, the students figure out how events affect GDP. My students have found this activity extremely beneficial to them in the past.

-Michael Melvin

Something I found very useful at the start of my Macro unit was to talk to my students about the political spectrum. I was always a little shocked to learn that many of my students did not really know the difference between conservativism and liberalism when it came to economic matters. Having a better understanding of the "isms" allowed my students to see more clearly why politician A wants to do this with the economy while politician B wants to do that with the economy.

-Mike Raymer

Mar 4, 2009

County by County

If you look at just one interactive unemployment map today please make it this one. If I was still in the classroom I would project this thing nice and big with my LCD projector. I would then locate the county where my students lived. Next I would compare my county rates to surrounding county rates. I would then click on the counties that have the highest unemployment rates in the country (I'm looking at you Imperial County!) and ask my students to explain why certain areas have higher rates of unemployment than others.

If you look at just one interactive unemployment map today please make it this one. If I was still in the classroom I would project this thing nice and big with my LCD projector. I would then locate the county where my students lived. Next I would compare my county rates to surrounding county rates. I would then click on the counties that have the highest unemployment rates in the country (I'm looking at you Imperial County!) and ask my students to explain why certain areas have higher rates of unemployment than others.Another cool thing I would do would be to compare current unemployment rates with the rates from one year ago. How much have the rates changed? Why have some areas been hit harder than others. And on and on and on...

This may be one of the coolest interactive maps I have seen in a long time. Let me know what your students think.

Mar 3, 2009

Something to Ponder

"The American International Group’s conference call just ended. The chief executive, Edward Liddy, seemed a little defensive, and for good reason.

"The American International Group’s conference call just ended. The chief executive, Edward Liddy, seemed a little defensive, and for good reason.In the fourth quarter, A.I.G. said it lost $61.7 billion. That amounts to $465,421 a minute. To put that in perspective, every six seconds it loses enough to pay full tuition for a year at Harvard."

-Floyd Norris, NYTimes

From the Classroom vol 9

Just a quick note here a week or so before my micro test about the Econ EOCT that the state has released. It can certainly be used as a study aid at the end of the semester, but I like to incorporate questions from this test into my own tests. And it should be remembered that the standards have changed a bit since this test was administered, but it is nice to have as many tools available as possible.

Mar 1, 2009

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Subscribe to:

Posts (Atom)